The MPC decided to keep all rates unchanged as expected. In a welcome relief at least to certain quarters of the market, it persisted with its time based dovish forward guidance as well.

Market Was Fearful…

The market had gone into the December policy on a slightly fearful note. This had been brought about largely owing to a confluence of 3 factors: One, local CPI inflation has been frustratingly sticky with decided signs of broad-basing amongst underlying components. Two, there is a global reflation trade in play as evidenced in sharp spikes in asset and commodity prices. India’s economic data over recent months has also been better than initially feared thus prompting GDP upgrades almost across the spectrum of analysts, Three, largely owing to large incoming dollars over the past few weeks which were getting aggressively absorbed by RBI, core system liquidity has spiked to greater than INR 8 lakh crores thereby dragging front end to levels meaningfully lower than the reverse repo rate. Basis these, there was a view that the RBI may announce steps to re-anchor the overnight rate closer to the reverse repo rate. The fear was that in doing so, it may end up signaling some sort of a reversal to the level of accommodation that is currently in play.

…But Inertia Still In Play…

As it turned out, policy has shown an inertia that is welcome in our view. No measures have been announced for now to re-anchor the overnight rate. While pressures on inflation have been noted, the predominant imperative of nurturing growth impulses at this juncture is well articulated. Instead, for now, the government is being nudged to use the small window that “is available for proactive supply management strategies to break the inflation spiral being fuelled by supply chain disruptions, excessive margins and indirect taxes”, while monetary policy is committing to “monitor closely all threats to price stability to anchor broader macroeconomic and financial stability”.

…For Now

In our view, a somewhat common policy theme across major economies is to not just focus on the recovery currently underway (which has been somewhat sharper than expected) but whether it will prove to be durable once the pent-up demand plays out. It is also concerned with mitigating the longer term damage or permanent scarring that is almost definitely in the process of getting created. Markets, on the other hand, have shorter horizons and respond more actively to concurrently evolving dynamics. A similar dynamic seems to have been in play with respect to India’s monetary policy assessment as well. Thus from the RBI/MPC standpoint, the need is to ensure that financial conditions remain accommodative so that credit flow may receive the necessary incentive to support the incipient recovery that is in play. This is especially so as the fiscal response in India has been quite measured thus far and may not be a key pillar for the revival in aggregate demand.

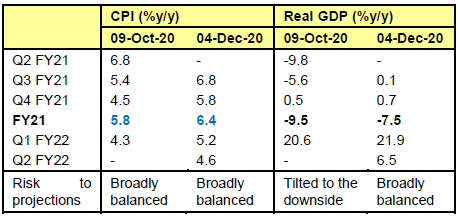

However, there are limits to patience as well especially in an emerging market context and where the ‘peace’ won with inflation is one of recent origin. So while the government’s contribution to aggregate demand has been modest so far as noted above, the MPC is also urging it to fix the supply side issues that are contributing to the high and sticky inflation. Should these measures be forthcoming, the MPC / RBI can comfortably continue with the primary mandate of supporting growth via easy financial conditions. It is also to be noted that the bar for changing the current commitment of monetary policy still seems to be high given the current assessment that inflation is largely a supply side issue that will eventually be resolved. However, there is nevertheless a policy ask here that the government needs to meet for continuation of the current level of accommodation for an extended period of time. This is also looking at the evolution of the growth forecasts from RBI as detailed below.

Source: RBI. Note: Full year CPI for FY21 is derived as the average of quarterly actuals available and RBI projections.

Takeaways and Implications

With the market’s mind relieved for now on the overnight anchor, interest with respect to front end rates should get re-established. It is to be noted also that one cannot think of policy in binary terms. A more fruitful approach probably is to envisage that some gentle (and hopefully non disruptive) reversals to the level of overnight rates is to be expected over the next year or so, even as the process hasn’t started with the December policy. This should be viewed as a transition of monetary policy from emergency support levels currently to a more sustainable level where it is still relatively accommodative in light of the weaker trajectory of growth in the ‘new normal’ that may lie ahead. Put in the bond market’s perspective, the current difference between 10 year bond yield to overnight rate is roughly around 300 bps. This will likely fall over the year ahead, although it will still be higher than the last few years’ average given higher continued fiscal stress as well as likelihood of relatively accommodative monetary policy. It is also very likely that, given the system is operating at even below the reverse repo rate, the bulk of this adjustment will be made by the very front end. This is not to say that long end rates won’t have to adjust. Rather, the quantum of adjustment there may be of a relatively smaller magnitude when compared with rates at the very front end. It is also to be noted that such adjustments are likely to be gradual and the ground to cover till normalization, at least till the first such equilibrium, may not be anywhere as large as has been the case in previous such episodes of very low front end rates.

The above dynamic, and how best to play it, will likely be a dominant feature of bond markets going forward. There are two important considerations here, in our view: One, the decision cannot be to sell everything and sit on cash. This is because, as noted above, the pace of normalization may be slow. In the meanwhile, given the steepness of the curve, the ‘carry loss’ embedded as the cost of waiting is quite meaningful. Two, unlike in ‘normal’ times when the yield curve is quite flat the decision on duration isn’t a binary one any more. Rather, the fund manager has to examine the steepness of the curve and position at points where the carry adjusted for duration seems to be the most optimal. That is to say, even if yields are to go up there are points on the curve where the extra carry compensates enough for a limited rise in yields so that the trade still earns better than the rate on offer on (let’s say) 1 year treasury bills today. Whereas if such a rise were to not materialize, then returns from the trade could be considerably more. It is such nuances that we are considering quite actively in the current context. Consistent with this, we have reverted to an overweight position in our long preferred 6 – 9 year segment in government bonds, in our actively managed duration products. Again, these are active mandates and strategy can change at any time.

Disclaimer:

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

The Disclosures of opinions/in house views/strategy incorporated herein is provided solely to enhance the transparency about the investment strategy / theme of the Scheme and should not be treated as endorsement of the views / opinions or as an investment advice. This document should not be construed as a research report or a recommendation to buy or sell any security. This document has been prepared on the basis of information, which is already available in publicly accessible media or developed through analysis of IDFC Mutual Fund. The information/ views / opinions provided is for informative purpose only and may have ceased to be current by the time it may reach the recipient, which should be taken into account before interpreting this document. The recipient should note and understand that the information provided above may not contain all the material aspects relevant for making an investment decision and the security may or may not continue to form part of the scheme’s portfolio in future. Investors are advised to consult their own investment advisor before making any investment decision in light of their risk appetite, investment goals and horizon. The decision of the Investment Manager may not always be profitable; as such decisions are based on the prevailing market conditions and the understanding of the Investment Manager. Actual market movements may vary from the anticipated trends. This information is subject to change without any prior notice. The Company reserves the right to make modifications and alterations to this statement as may be required from time to time. Neither IDFC Mutual Fund / IDFC AMC Trustee Co. Ltd./ IDFC Asset Management Co. Ltd nor IDFC, its Directors or representatives shall be liable for any damages whether direct or indirect, incidental, punitive special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information.