The intent of the FY23 union budget is to nurture growth, primarily through public investment, as private investment is yet to meaningfully pick up. It continued to be more transparent, by reducing off-budget expenditure, and relatively conservative in its estimates of receipts. The two numbers which really stood out were the higher capex and higher market borrowing for FY23. We look at the tradeoffs of this approach, in terms of its likely impact on states, funding, fiscal consolidation and, most importantly, growth.

Conservative or realistic estimates?

Implied Q4 FY22 (Jan-Mar) estimate point to a 14.5% y/y contraction in gross tax revenue, after it grew 44% during Apr-Dec. Revenue from excise duties (which fall given the cut in November 2021), income tax, CGST, etc. appear realistic. However, corporate tax revenue estimate is quite conservative at ~0.3% of GDP below our forecast, which could help ease the final FY22 fiscal deficit. Net tax revenue in Q4 FY22 is estimated to fall 37% y/y also because tax devolution to states is estimated to grow 32% y/y.

For FY23, nominal GDP at 11.1% is quite conservative and overall tax buoyancies are estimated to moderate from FY22 as expected. Direct tax buoyancy is estimated to fall slightly blow pre-pandemic levels while indirect tax buoyancy is different also owing to excise duty cuts, changes in the GST system, etc. Overall, FY23 gross tax revenue growth estimate of 9.6% is towards the lower end of realistic outcomes. The scope for surprise is thus to the upside, mainly from corporate tax revenue, although not to the extent seen in FY22 as pent-up demand diminishes and further buoyancy from higher GST compliance could be lower. The likely macroeconomic context ahead – slower global growth and trade, global monetary policy normalisation, slower Chinese economy, impact of higher oil prices, incomplete recovery of the domestic services sector, health of households given the K-shaped recovery, etc. – could also limit the upside.

Capex growth – details matter as always

On-budget capex is estimated to rise by 24.5%y/y to Rs. 7.5 lakh crore in FY23, from an upward revised Rs. 6.03 lakh crore in FY22 which itself is a 41.4% rise. This is encouraging as share of capex in total on-budget expenditure (measure of quality of spending) rises consistently (Figure 1). However, like last year, off-budget capex eases. In FY22, this is broad-based across 7-8 ministries while in FY23 it is mainly on-budgeting of support (Rs. 65,000cr) to the National Highways Authority of India. This is indeed good for transparency but reduces consolidated capex. There are also some one-offs like the loan to railways in FY21 (Rs. 79,398cr), clearing of Air India liabilities in FY22 (Rs. 51,971cr) and special assistance through fifty-year interest-free loan to states for capex (Rs. 11,830cr in FY21 and Rs. 15,000cr in FY22 which rises to Rs. 1 lakh crore in FY23). To be fair, states’ capex could rise by the loan amount but timely execution matters for eventual off-take. The actual growth in capex and thus the impetus to growth could be lower than what the headline numbers suggest.

Figure 1: Adjusted capex growth

Funding the deficit through higher market borrowing – trade-off for higher capex

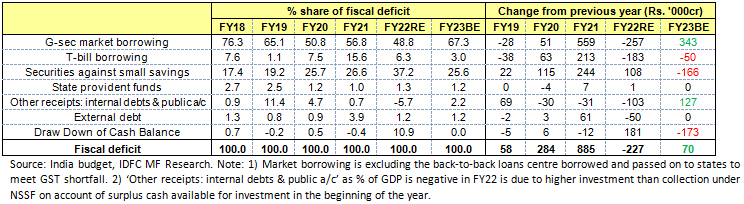

Figure 2: Higher share of market borrowing in FY23 but there is scope for a mild surprise

The tradeoff for higher capex in FY23 is the higher share of market borrowing in fiscal deficit which, after falling from 76% in FY18 to 49% in FY22, picks up sharply to 67% in FY23. This is primarily owing to lower utilization of cash balance and lower short-term borrowing vs. FY22. Funding from NSSF a) through ‘securities against small savings’ falls in FY23 after picking up in FY22 but b) through its core inflows (savings deposits, savings certificate and public provident fund) picks up.

However, a) lower FY23 fiscal deficit, b) higher cash utilization (our estimate of central government cash balance is Rs. 4.84 lakh crore as on 21 January 2022) and c) recent G-sec switches with the RBI which reduced FY23 redemption by Rs. 63,648cr offers scope for a mild relief to the Rs.14.95 lakh crore gross borrowing announced in the budget.

However, total public sector deficit (defined as centre’s fiscal deficit + states’ fiscal deficit + Resources of PSEs excluding internal resources) has come off from recent highs (10.3% of GDP as per FY23BE vs. 15.8% in FY21) but is still well above 8.1% in FY19. There is risk of this crowding out private investment once it starts to pick up down the line.

States – bigger role in capex but conditions apply

States’ revenue from tax devolution has been falling, given increase in central excise duties on fuels which are not shareable and, more recently, from falling share of customs (Figure 3).

Figure 3: Lower share of states in tax devolved

Compensation provided to states, from cess collected, for shortfall in GST collection ends in July 2022 and loans provided were for FY21 and FY22. States were allowed additional market borrowing, partly conditional on reforms and capex, and carried forward space expired in FY22. For FY23, states have been allowed a fiscal deficit of 4% of GSDP, again 0.5% of which is tied to power sector reforms. They will also be provided with 50-year interest-free loans worth Rs. 1 lakh crore for capex.

All this is definitely a good way to incentivise states to undertake important but difficult reforms, like in the power sector, and direct limited resources to capex with higher growth-multiplier and lower inflation outcomes. However, cooperation from all states, their ability to timely manage revenue expenditure (given a higher share of conditional inflows) and the need to account for differences among states in priority and avenues of spending (which a common mandate could miss) must also be taken into consideration. Impact on state spending (~55-60% share each in consolidated revenue and capex) thus borrowing has to be seen given states had already announced a larger-than-expected Q4 FY22 borrowing calendar, GST-related support is about to end and borrowing costs have been rising more recently. FY23 state budgets, due in the next few months, should provide some indication. Overall, states now have a larger and clearer role in capex and reforms, albeit with the centre directing a bigger share of resources.

Fiscal consolidation – what it takes to be on the glide path

Centre’s fiscal deficit is targeted at below-4.5% of GDP by FY26. If one does a basic exercise on forecasting major receipts and expenditure till FY26, need for a broader pick up in sources of receipts becomes immediately clear. In other words, non-tax revenue (RBI dividends, telecom spectrum related receipts, etc.) and/or non-debt capital receipts (disinvestments) need to step up soon. This is also because our pre-pandemic growth was already slowing (FY20 real GDP growth was recently revised downward from 4% to 3.7%) and our potential growth has been likely hit by economic scarring and a K-shaped recovery in the absence of a meaningful employment and wage cycle in the last wo years. Growth (and thus capex for it) is thus good to stabilize the fiscal deficit to GDP ratio but we still need non-tax receipts to fire to be on the glide path.

Despite the tradeoffs, can public investment get the economy’s wheels moving?

Capex-led impetus for growth is likely a good option now given balance sheets of corporates and banks are likely better on aggregate, although possibly with skews within. However, capacity utilisation broadly continues to be at levels below thresholds to commence a private capex cycle. Balance sheets of households on aggregate (impacted in the last decade by the investment slowdown percolating onto the demand side but then staying afloat with leverage from NBFCs until 2018 after which private consumption materially slowed and is currently below the pre-pandemic real level) have also likely been hit again by the pandemic and the following K-shaped recovery. With these constraints in play, execution, quality of expenditure and getting states fully on board becomes even more critical to generate inclusive medium-term growth. However, the funding route taken for this in the immediate future tests the appetite of the domestic bond market, although there could potentially be some mild positive surprise here as we traverse FY23.

Disclaimer:

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

The Disclosures of opinions/in house views/strategy incorporated herein is provided solely to enhance the transparency about the investment strategy / theme of the Scheme and should not be treated as endorsement of the views / opinions or as an investment advice. This document should not be construed as a research report or a recommendation to buy or sell any security. This document has been prepared on the basis of information, which is already available in publicly accessible media or developed through analysis of IDFC Mutual Fund. The information/ views / opinions provided is for informative purpose only and may have ceased to be current by the time it may reach the recipient, which should be taken into account before interpreting this document. The recipient should note and understand that the information provided above may not contain all the material aspects relevant for making an investment decision and the security may or may not continue to form part of the scheme’s portfolio in future. Investors are advised to consult their own investment advisor before making any investment decision in light of their risk appetite, investment goals and horizon. The decision of the Investment Manager may not always be profitable; as such decisions are based on the prevailing market conditions and the understanding of the Investment Manager. Actual market movements may vary from the anticipated trends. This information is subject to change without any prior notice. The Company reserves the right to make modifications and alterations to this statement as may be required from time to time. Neither IDFC Mutual Fund / IDFC AMC Trustee Co. Ltd./ IDFC Asset Management Co. Ltd nor IDFC, its Directors or representatives shall be liable for any damages whether direct or indirect, incidental, punitive special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information.