The February policy review kept all rates unchanged as well as the accommodative stance maintained, with the usual one dissent. It was more dovish than market assessment in 1> not taking any step whatsoever towards corridor normalization (no hike in reverse repo rate), 2> providing some line of sight that the accommodative stance may continue for a while, and 3> sounding quite dovish on the growth – inflation assessment (second half FY23 inflation forecast seems much below market expectations).

Analytical Boldness

The minutes of the December RBI policy were particularly noteworthy for us. It elaborated upon the analytical framework underpinning the somewhat ‘relaxed’ stance of RBI and suggested that there is hence likely to be some ‘shelf-life’ to the dovishness (https://idfcmf.com/article/6632 ). RBI’s analysis, as represented by Dr. Patra’s minutes then and included in our note referred to in the link here, made the following notable observations:

1> Despite recent growth pick up economic activity generally has only approached 2019 levels which itself represented the culmination of a multi-year growth slowdown. Additionally, global growth momentum seems to be slowing and new Covid concerns have risen, thereby threatening to put paid to what is already an incomplete recovery with substantial scarring from the pandemic slowdown.

2> Inflation is a worry for now, especially with some pass throughs and price hikes still pending. However, this will likely subside by second half of 2022 as the so-called ‘bull-whip’ starts moving in the reverse direction for global supply chains. The first signs of this happening may already be there with some build up being seen in product inventories in manufacturing surveys.

3> There is stated inclination to ‘take guard and resume battle readiness again’ in the face of the new virus variant./span>

The policy today stayed consistent with the above and in fact built upon the points mentioned. The Governor in his statement noted that output is just barely above its pre-pandemic level, while private consumption is still lagging; even as global headwinds are accentuating. Also, the monetary policy committee (MPC) statement observed that available high frequency indicators suggest some weakening of demand in January 2022 reflecting the drag on contact-intensive services from the fast spread of the Omicron variant in the country. This ties up almost exactly with Dr. Patra’s December minutes.

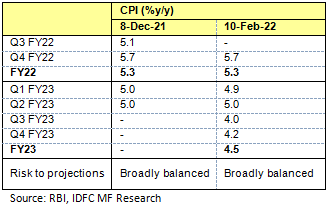

The same consistency, in fact in a much starker fashion, is seen in the inflation assessment in this policy. The table below summarizes RBI’s inflation assessment till the end of FY23.

The large difference between RBI and private sector forecasts for CPI evolution in FY23 lies in the second half financial year’s trajectory, where the central bank’s forecast is much lower. This likely takes into account the ‘bull-whip’ effect referred to by Dr. Patra in December. This may not be getting modelled into private sector forecasts, at least not to the same extent. In the media press conference, RBI leadership repeatedly referred to them having taken into account risks from commodities etc. and the fact that responsible projections are a matter of credibility for the central bank.

The important point here is this: RBI’s defense that it is not behind the curve comes from their own rigorous analysis and forecast on the likely inflation trajectory ahead. This assessment is markedly different from most of the private sector forecasts. It is then a matter really about who turns out to be right on the assessment eventually. If RBI turns out to be right, then its current path of policy may be exactly the thing that needed to be done. This is especially true if the relatively responsible aggregate policy reaction in India (fiscal plus monetary) in response to the pandemic is kept in mind.

On the flip side, the central bank is running an obvious risk of its forecast being wrong. However, to be fair, it isn’t that there are no ‘hedges’ it has put in place. Thus, as the Governor noted, the ‘effective reverse repo rate’ has increased by 50 bps since end August courtesy the VRRR tool (thought with attendant distortions for non-banks that we have referred to before). Also, a notable change in RBI’s response function over the pandemic period has been its aggressive stance in accumulating forex reserves. It must also be seeing this as a considerable ‘uncertainty buffer’ as well, including from global spillovers.

Global Linkages

Even in December, RBI leadership clearly drew a distinction between macro-dynamics in the US versus ours. In fact, a noteworthy point in the February policy as well is that in the central bank’s analytical framework global financial conditions tightening seems to have more relevance as a downside risk to growth rather than pose a considerable financial stability risk for us. In the post policy media call, RBI leadership team again emphasized on the point that the characterization of inflation in India is very different from that in the Western world. To be clear, this doesn’t mean that markets and RBI should ignore global developments. However, RBI’s point seem to be that this also doesn’t mean that global developments should start to dominate local factors in policy making. This is also especially true as, as noted by the Governor, monetary policies in the largest and the second largest economy are in fact moving in opposite directions.

Again, there is an element of risk that RBI is taking in this assessment; especially in context of the recent widening in the current account deficit. But as in the case of the growth-inflation discussion above, this seems to be calculated and well thought out and isn’t without some hedges available (high forex buffer).

Market Dynamics

Overnight rates will likely remain volatile as the revised liquidity framework progresses; now with the addition of term variable rate repos (VRRs). Thus, while there is now much more comfort that a repo rate hike is far away, money market rates will still have to battle the uncertainty of fluctuating rate of overnight deployment for non- bank participants like mutual funds. For bonds, while there is no quantifiable commitment on imminent explicit support, there are still nevertheless important takeaways. One, the Governor has repeated the desire for orderly evolution of the curve, and the need for market participants to be responsible. Presumably this doesn’t imply only a one-sided commitment and entails action from RBI as well, even though not pre-committed. Two, the voluntary retention route (VRR) scheme for FPI participation in bonds has been further enhanced by INR 1 lakh crores. Three, the Governor noted that market’s perception of inflation (and the unsaid interpretation therefore of extent of RBI tightening) may have been too pessimistic. Some unwind here is getting reflected in a notable 20 bps fall in 1 year swap rates at the time of writing. Four, he reaffirmed the view expressed by others as well that government borrowing may be getting exaggerated owing to a variety of reasons.

In summary then, with market expectations of a repo rate hike now getting reasonably pushed back, the demand for carry likely comes back. This is getting reflected already in the bull-steepening of the yield curve today. Thus, a bar-bell strategy that over-weights the 4 – 5 year (our preferred overweight segment) gets extra appeal post this policy. Put another way, even with some mark-to-market volatility assumed, the opportunity loss in holding cash now is higher given the expectation of further delayed repo rate hike after this policy. Longer duration bonds (10 year and beyond) however, still don’t have a definitive trigger and will have to await a more sustainable resolution of the medium term demand-supply equation for bonds.

Given the above, we reiterate our preference for overweight stance in the 4 – 5 year government bonds. As always this represents our current thinking and stance. A related point to ponder is that while we need to proceed with a working assumption of how many rate hikes happen ahead, it is more and more apparent that the market may be reasonably overestimating this trajectory. This is especially true given our current expectation that global growth drivers don’t seem sustainable (remember US has led global growth in the past year or so on the back of an unsustainably large fiscal stimulus which is now fading). On top of this, if RBI’s second half inflation trajectory turns out to be close to the truth then we may just find out that this rate normalization cycle has much weaker legs that what is generally built into market expectations currently.

Disclaimer:

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

The Disclosures of opinions/in house views/strategy incorporated herein is provided solely to enhance the transparency about the investment strategy / theme of the Scheme and should not be treated as endorsement of the views / opinions or as an investment advice. This document should not be construed as a research report or a recommendation to buy or sell any security. This document has been prepared on the basis of information, which is already available in publicly accessible media or developed through analysis of IDFC Mutual Fund. The information/ views / opinions provided is for informative purpose only and may have ceased to be current by the time it may reach the recipient, which should be taken into account before interpreting this document. The recipient should note and understand that the information provided above may not contain all the material aspects relevant for making an investment decision and the security may or may not continue to form part of the scheme’s portfolio in future. Investors are advised to consult their own investment advisor before making any investment decision in light of their risk appetite, investment goals and horizon. The decision of the Investment Manager may not always be profitable; as such decisions are based on the prevailing market conditions and the understanding of the Investment Manager. Actual market movements may vary from the anticipated trends. This information is subject to change without any prior notice. The Company reserves the right to make modifications and alterations to this statement as may be required from time to time. Neither IDFC Mutual Fund / IDFC AMC Trustee Co. Ltd./ IDFC Asset Management Co. Ltd nor IDFC, its Directors or representatives shall be liable for any damages whether direct or indirect, incidental, punitive special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information.