Our reading of RBI’s characterisation from the last two policies was that it considered the total monetary and fiscal responses in India since the pandemic as being largely modest, saw growth drivers still being quite weak, and was happy to characterise the incremental supply pressures as largely supply side with not much ‘second’ order effects in play. Hence this view was comfortable with the pace of tightening thus far (effective overnight rate hike via VRRR, recent balance sheet shrinkage). Then there came a major geo-political event putting major upward pressure on global commodities, further pressuring supply chains, and also with reasonable detrimental effects on growth. This had materially pushed higher inflation expectations around the world. Wherever inflation dynamics where already tight, the primarily example being US, policy tightening expectations have been significantly ratcheted up. In India, where the going in view from RBI was leaning more worries on growth vis-à-vis inflation, our view (supported somewhat by a speech by Dr. Patra in March: “While the fallout of the geopolitical situation is being assessed and will be factored into our projections, it is reasonable to treat it as a supply shock at this stage in the setting of monetary policy”) was that even though the inflation forecast will have to be revised higher, the characterisation of inflation and the order of worries for RBI may remain the same as before.

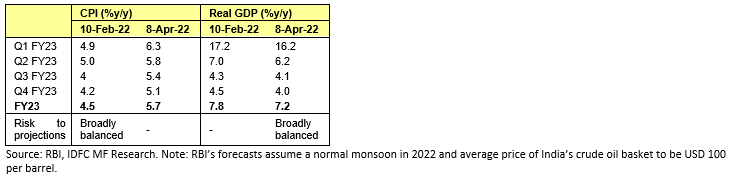

The revised projections as summarised above have indeed been material, much more so for inflation as compared with growth. This partly also reflects the fact that the earlier assessment for second half FY23 seemed materially lower than that of the market. This is now corrected, even as market forecast has moved up even more to accommodate for the latest commodity shock and the possible extension of supply chain congestions. It is probably this larger inflation revision as well as the unusually high uncertainties in the environment that the geopolitical escalation has brought, that has led to what is fairly described as a pivot with RBI.

The Contours of the Pivot

Governor Das mentioned in the press conference clearly that the inflation revision is on account of war induced factors (crude oil, edible oil, wheat, feed costs). These are all essentially supply shocks but still are large in magnitude. This is also evidenced in the fact that even as per RBI’s forecast (and taking into actual inflation outcomes calendar year to date), we are going to be within a whisker of 6% getting breached for 3 consecutive quarters. Thus it made sense for RBI / MPC to probably get some leeway for itself. And so the guidance on remaining accommodative ‘while focussing on withdrawal of accommodation to ensure that inflation remains within the target going forward, while supporting growth’, made sense. This was paired with a distinct assurance in the Governor’s statement that RBI would engage in a ‘gradual and calibrated withdrawal’ of liquidity over a ‘multi-year time frame in a non-disruptive manner beginning this year’. Further a standing deposit facility (SDF) has been introduced at 3.75%, thereby putting the corridor at a 50 bps spread when defined between the two uncollateralised rates of Marginal Standing Facility (MSF) and SDF. Given that the VRRRs were already nudging effective deployment rates for banks higher, this also could be positioned largely as an operational adjustment; with the added benefit of increasing flexibility for future liquidity absorption without the burden of having enough corresponding collateral.

Where things went somewhat ‘stickier’, or the pivot got hardened, is in the post policy media interaction. The Governor was specific here in mentioning that RBI’s order of priorities is now inflation before growth. The length of this statement does no justice to how potentially loaded it can be. Even with the revised forecast, most market participants will still believe that risks of FY23 projection at 5.7% are to the upside. Why the expectation was that this wouldn’t invite more rate hikes was owing to RBI’s previously stated order of worries and the potential characterisation of inflation. However, Governor’s statement throws this assessment into chaos, so that market is free to price in rate hikes basis largely inflation assessment alone going ahead. Then Dr. Patra weighed in with some comments on real policy rates. Basically, the point made seemed that zero real repo rate (4% repo versus same targeted inflation) corresponded with an ultra-accommodative stance. So then presumably a movement to a lesser accommodative stance implies positive real repo rates. This in effect green-flags a possible hike in repo in the June policy itself. This expectation is also buttressed with the repeated comments from Das around the need to be flexible.

While the immediate market price action reflects a lot of positioning pains, nevertheless it is noteworthy today. Swap yields are up 30 – 40 bps. This is over and above an already reasonably large rate hike cycle that they were already pricing. Apart from positional dynamics as alluded to before, this also reflects an inability of the market (basis last received RBI commentary) to have any sort of a reasonable handle on the upcoming RBI response function.

Going Forward

Our own underlying framework has suffered a setback with today’s policy. The policy de-emphasizes the relative importance of growth and thus changes the context (for now) in which to look at additional growth worries emerging around the world. It puts prospects of a repo rate hike very much on the table for June. Further, it provides a somewhat more ‘panicky’ lens with which to view any upward surprises in either commodity prices or in near inflation prints. What is noteworthy from the swap curve mentioned above is that the steepness of the curve hasn’t offered much protection today. As an example, the 1 year swap is pricing close to 5.5% as effective overnight rate by end of year (or repo rate hike in every policy over the year) and the 1 year swap 1 year forward is at something like 6.25%.

Given the policy description today, it is prudent to budget for quicker normalisation than previously envisaged. However, we are still reluctant to yet alter our general expectation of a lower terminal overnight rate in this cycle versus the last. This view also follows from our expectation that this isn’t likely to be a normal, long drawn cycle allowing for a very long normalization runway. This now looks even more likely given the aggressive pace of expected monetary policy tightening in the US, the growth damage from the ongoing geopolitical escalations, and the new Chinese slowdown on the back of a renewed Covid outbreak. Thus, we think even as RBI may begin well, it may not get as far in the normalisation cycle as the swap curves are currently pricing. That said, we also recognise that it is hard to push against market pricing in the immediate term.

There is near pain in our portfolio strategies: barbell with an overweight around 4 years. This is because, as noted in the context of the swap curve above, there is no protection from steepness when market’s assessment of possible RBI’s reaction function itself is thrown into chaos. However, as the dust settles we expect the carry-adjusted-for-duration to start to reassert itself. There is some ‘balm’ that has been offered in the form of 1% hike in held to maturity (HTM) limits of banks till March 23. Also, RBI’s open ended commitments remain on supporting the borrowing program and for the orderly evolution of the curve. These may all eventually help in stabilising market curves even as near term participants may seem more reluctant to assume risk. Investors who have the benefit of a longer horizon may want to continue scaling into strategies that optimise duration risk versus curve steepness. These should hold well over a period, given our views on this cycle as expressed above.

Disclaimer:

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

The Disclosures of opinions/in house views/strategy incorporated herein is provided solely to enhance the transparency about the investment strategy / theme of the Scheme and should not be treated as endorsement of the views / opinions or as an investment advice. This document should not be construed as a research report or a recommendation to buy or sell any security. This document has been prepared on the basis of information, which is already available in publicly accessible media or developed through analysis of IDFC Mutual Fund. The information/ views / opinions provided is for informative purpose only and may have ceased to be current by the time it may reach the recipient, which should be taken into account before interpreting this document. The recipient should note and understand that the information provided above may not contain all the material aspects relevant for making an investment decision and the security may or may not continue to form part of the scheme’s portfolio in future. Investors are advised to consult their own investment advisor before making any investment decision in light of their risk appetite, investment goals and horizon. The decision of the Investment Manager may not always be profitable; as such decisions are based on the prevailing market conditions and the understanding of the Investment Manager. Actual market movements may vary from the anticipated trends. This information is subject to change without any prior notice. The Company reserves the right to make modifications and alterations to this statement as may be required from time to time. Neither IDFC Mutual Fund / IDFC AMC Trustee Co. Ltd./ IDFC Asset Management Co. Ltd nor IDFC, its Directors or representatives shall be liable for any damages whether direct or indirect, incidental, punitive special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information.