The current budget is a part of 3-4 mini Budgets announced post the ‘Aatmanirbhar’ Package since May 2020 to sustain recovery. The focus of the current budget was to balance fiscal prudence with judicious spends to sustain the incipient recovery in the economy. As part of this exercise, off-balance sheet items (loans to Food Corporation of India (FCI) are now a part of the regular budget and hence improve the quality of fiscal math.

Broad contours of the Budget proposals and capital outlay themed under following structure:

- Aatmanirbhar Bharat programmes

- Performance-linked incentives

- Boost for domestic manufacturing

- Improved credit access for enterprises

- Moratorium on interest payments

- Thrust on affordable housing

- Booster shots for MNREGA

BUDGET MATH:

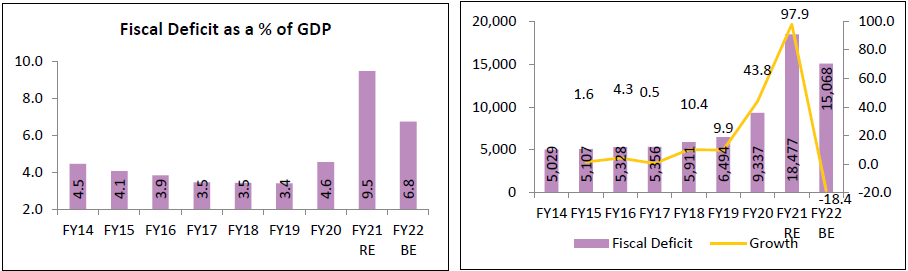

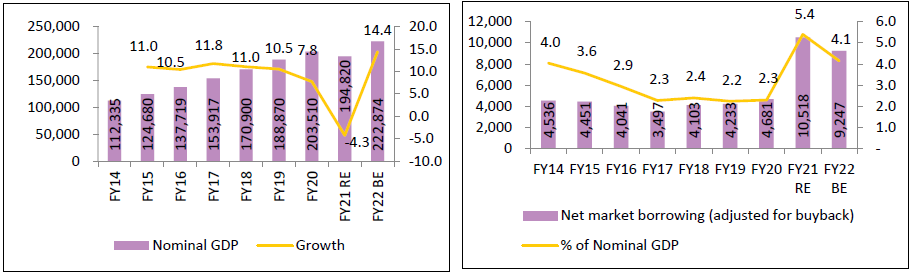

- Fiscal deficit estimates were a miss due to COVID-19 as it increased sharply to 9.5% of GDP v/s economist estimates of ~7-8%. Budget builds in 6.8% deficit for FY22 and then to follow a glide path to achieve 4.5% of GDP by FY26. Net market borrowing (adjusted for buyback) form 5.4% of the nominal GDP in FY21RE.

- Though the budget deficit may be highest ever, the fiscal math is far more believable. Even the glide path to reduce the fiscal deficit is moderate in its assumptions, a rarity in fiscal forecasts as compared to the past.

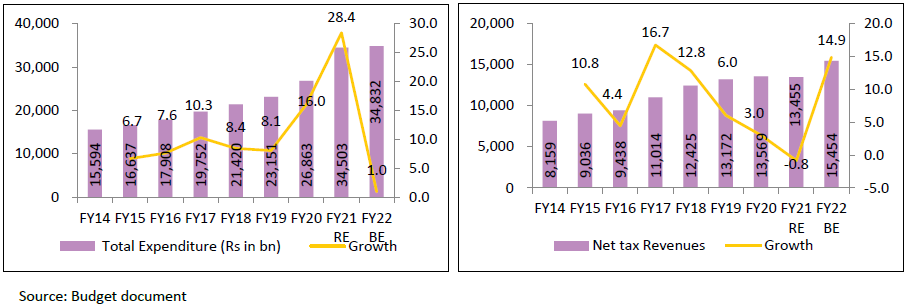

- Spike in Expenditure Growth for FY21RE is led by higher subsidies on Food and fertilizers, increased spends on agriculture and rural development and higher budget for railways. Due to pandemic, a perfect storm of higher expenditure and lower tax revenues have impacted the FY21 revised estimates. The Finance Minister has used the pandemic to “regularize” a few off balance sheet practices to improve the credibility of fiscal maths.

- As off-balance sheet items are now a part of the budget, total expenditure estimates increase by only 1% in FY22BE as against a nominal GDP rate growth of ~15%.

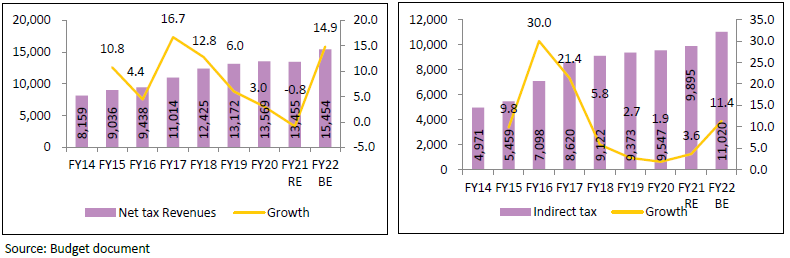

- With nominal GDP forecasted to grow at ~15%, revenue estimates look far more modest as compared to the past.

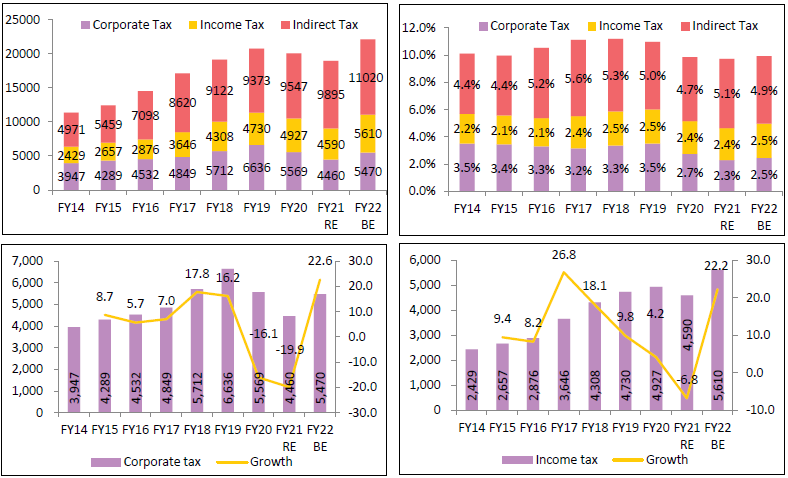

- Currently Nifty earnings estimates vary from 25-35% for FY22. In light of these estimates, the corporate tax collections at ~22.6% appears achievable.

- Even Indirect tax forecast at 11.4% in FY22BE is lower than the nominal GDP growth rate of ~15%.

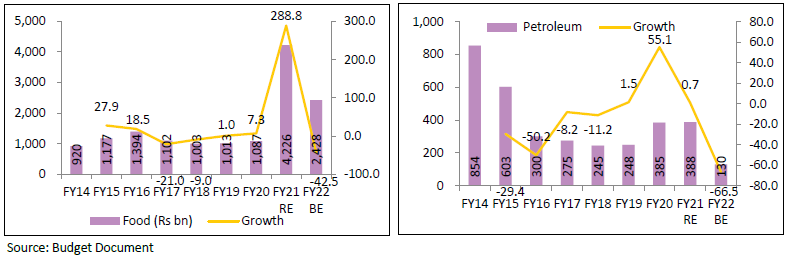

- As mentioned earlier, off-balance sheet items (loans to FCI) are now a part of the regular budget. This has led to a sharp increase in Food subsidy by 289% in FY21RE which then declines by 42.5% in FY22BE.

- India’s response to fiscal stimuli in the throes of the pandemic was more “measured” as compared to the developed countries like USA, Germany and Japan. MNREGA, was the preferred route in the stimulus, with outlay increasing to Rs 1,11,500 cr during FY21. This has “normalized” to Rs 73,000cr for FY22BE vs Rs 111,500cr. In addition, allocation to PMKSY has been almost doubled, albeit on a lower base while MGNREGA witnessed 13.4% reduction in allocation.

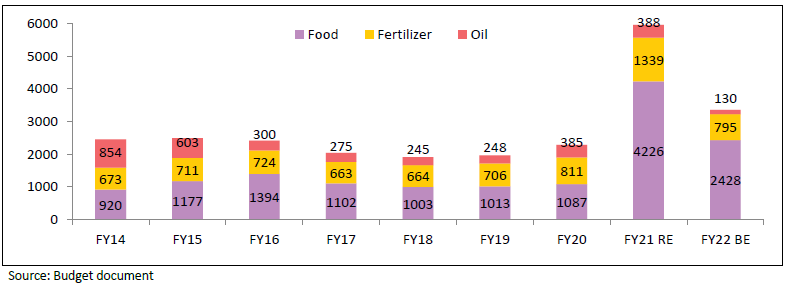

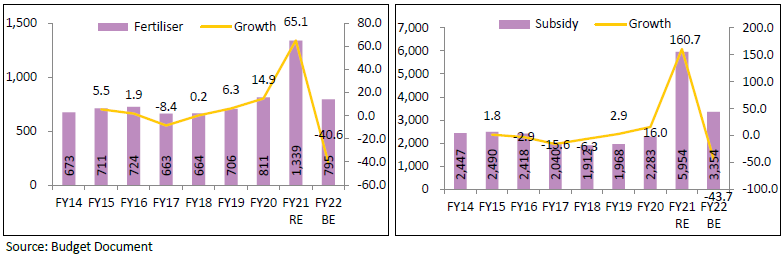

- Another highlight of the budget has been to cleanse the subsidies – Fertilizer; Food and Oil & Gas from a budget allocation perspective. All pending Fertilizer subsidy allocation for 2020-21, have been fully provided for, as a result the revised estimates stand at Rs 1,340bn (with an additional allocation of Rs 650bn announced during the year). Subsidy allocation for 2021-22 is at Rs 795bn. With this additional fertilizer subsidy, the entire subsidy backlog gets cleared in FY21. Similarly, Food subsidy is now part of the “regular” Budget and not an Off-balance sheet item. Oil subsidy remains low, as Oil marketing companies have been announcing frequent price hikes (too frequent, from a consumer’s point of view!)

Significant boost to Infrastructure sector

- Textile – Mega Investment Textile Park will be launched in addition to Production Linked Incentive Scheme (PLI) scheme. Plan to launch 7 such parks.

- National Infra Pipeline: Project pipeline now consist of over 7400 projects.

- Will introduce a bill to form Development Financial Institution (DFI) with Rs 200bn Capital

- National Asset Monetization Platform to be launched with a Monitoring via a dashboard – This will be used to monetize – Roads, T&D (transmission and distribution) Projects, DFC (Dedicated Freight Corridor) (after operational) and other assets by Railway, Airports, GAIL, IOCL (Indian Oil Corporation Ltd).

- FY22 CAPEX target stands at Rs 5.54tn v/s Rs 4.39tn. This is an increase of 35%. FY21BE had provided Rs4.12 lakh crores for capex and it will end at 4.39 lakh crore. Out of the above outlay, Rs2trn will be given to States and Autonomous bodies for CAPEX and will encourage them to do more.

- Roads: Gets Rs1.18 lakh tn for roads, Rs1.08tn of this amount is for Capex related spend.

- Asset Monetisation: National monetization pipeline to be launched with creation of an asset monetization dashboard to be created. Monetization shall happen for NHAI, PGCIL (Power Grid Corporation of India) etc. railways will monetize DFC, toll roads, Oil & Gas Pipeline (GAIL, IOCL, HPCL), airports (tier 2 & 3 cities), other railways infra assets, warehousing assets of CPSE, sports stadiums.

- Urban Infra: Raising the share of public transport through Metro and City Bus. New scheme will be launched at a cost of Rs 18k crore. It will facilitate deployment of innovative PPP models. Metro Light and Metro Neo will be deployed at lower cost in tier-2 cities and peripheral areas of tier-1 cities.

- Power: DISCOMs are monopolies and hence there was a need to provide a choice to consumer by promoting competition. A framework shall be put in place to give alternatives to consumers to choose from among more than 1 DISCOM. Revamped schemes for DISCOM will be launched with an outlay of more than Rs 3 lakh crore over five years.

- Petro & Natural Gas: Ujjwala scheme (8 crore beneficiaries) to be extended to cover 1 crore beneficiaries and 100 more districts to be added over next 3 years in CGD (City Gas Distribution). Also, Independent gas transport systems operator will be set-up for common carrier capacities

Health and Wellbeing

- Rs 350 bln towards purchase of Covid Vaccine with a promise to increase allocation if required. At Rs 250 / dose. This would budget for almost 700 mln dosages (per 2 dose).

- Rs 641.8bn to be invested over 6 years to improve primary, secondary and tertiary healthcare to strengthen the National Centre for Disease Control. Besides this, the government will also set up 15 Health Emergency Centres

- Total budget outlay for healthcare is Rs 2230bn an increase of 137% from last year with 17,000 rural and 11,000 urban health and wellness centres to be set up and integrated public health labs to set up in each district

- Urban Swachh Bharat 2.0 Mission to be launched at outlay of Rs1410bn over 5 years

- Jal Jeevan Mission for urban- Aims at universal water supply in all 4,378 Urban Local Bodies with 2.86 crores household tap connections, as well as liquid waste management in 500 AMRUT cities. It will be implemented over 5 years, with an outlay of Rs 2,87,000 crores.

Agriculture and Rural

- Agriculture credit target enhanced to Rs 16,500bn with credit focus towards animal husbandry, dairy and fisheries.

- Allocation towards rural infrastructure development fund from Rs 300bn to Rs 400bn.

- Doubled allocation of micro irrigation fund under NABARD from Rs 50bn to Rs 100bn

- 1000 more mandis will be integrated with e-NAM to have transparency and competitiveness.

- Custom duty on urea, di-ammonium phosphate (DAP) and muriate of potash (MOP) (major product of imports) reduce to nil (from 5%) and Agri infra cess is introduce at 5%. So, no changes or impact

- Fertilizer subsidy allocation for 2020-21 was revised at Rs 1,340bn (with additional allocation of Rs 650bn announced during the year). Subsidy allocation for 2021-22 is at Rs 795bn.

- Crude Palm Oil: Duty increased from 27.5% to 32.5% (BCD (Basic Customs duty) of 15% and Agriculture Infrastructure and Development Cess (AIDC) of 17.5%)

- Crude Soyabean and Sunflower seed oil duty of 15% and AIDC of 20%

- For cotton BCD of 5% and AIDC of 5%

Phased manufacturing plan for electronics products and components

Similar to last budget, they continue to see BCD hikes:

- Compressor (AC, Refrigerators) from 12.5% to 15% – Most of the compressors for AC/Refrigerators are imported (less than 20% is domestic manufacturing). This is aimed to spur domestic manufacture of this vital component, given the large capital spend required, hiking Custom Duty offers “protection” in initial years from well-established imports.

- Specified insulted wires and cables from 7.5% to 10%

- Inputs and Parts of LED lights and fixtures from 5% to 10%- these are largely imported

- Solar inverters from 5% to 20%

- Inputs to Printed Circuit Boards (PCBs), camera module & connectors in mobile phone hiked to 2.5% from nil

- PCB and molded plastic for chargers and adaptor hiked from 10% to 15%

- Inputs for mobile charger hiked from nil to 10%

Positive: Personal Income Tax remains stable; Not many benefits given but NO COVID CESS also

- No tax returns for Senior Citizens of age 75 years and above who have only pension and interest income

- To ease compliance for taxpayers, Income Tax returns will have prefilled data from capital gains also.

- Faceless Income tax Appellate Tribunals National faceless ITAT center to be set up

- Reduce time limit for reopening of tax assessments to 3 years. Reduction in Time for Income Tax Proceedings. Presently, an assessment can be opened in 6 years, and in serious tax fraud cases for up to 10 years.

- The threshold for serious tax frauds is pegged at Rs 5mn above which assessment can be done upto 10 years. This is a big relief for many HNI and HUFs in India

- Tax Audit threshold of turnover further increased for digital transactions to Rs 10cr from Rs 5cr. This shall ease compliance burden for small companies

- Dispute Resolution Panel for small taxpayers

- Dividend to REIT & INVT are exempt from TDS

- Proposal for Tax exemptions for aircraft leasing cos

- Advance tax on dividend to accrue only after it is declared.

- Affordable housing is a priority area Rs1.5 lakh for loans to purchase affordable house is now extended by one more year

- To enable deduction of tax on dividend income at lower treaty rates for FPIs

- Misuse of EPF to earn “assured” 8% tax free return plugged. With EPF contribution upto Rs 2.5 Lakh per annum exempt from tax.

Other announcements

- Plan to sell Government’s IDBI Bank stake. Further 2 more public banks and 1 public insurance company to be privatized in FY22

- Plan to sell part of holding in LIC in IPO in FY22 itself

- Strong emphasis on affordable housing continues

- Timebound announcements of AD (anti-dumping duty) and CVD (Countervailing duty)

- No hikes in National Calamity Contingent Duty (NCCD) or excise on Cigarettes

- Agriculture Infrastructure and Development Cess (AIDC) of 100% has been levied on Alcohol Beverages (brandy, bourbon, whiskey, scotch, etc.). Simultaneously, the BCD has been reduced to 50% from 150%. Thereby, net impact seems to be Neutral.

- Positive for Jewellery industry: Customs duty on Gold and precious metals decreased from 12.5% to 10% (7.5% BCD + 2.5% cess) – this will enable volume growth

- Positive for domestic leather and leather product manufacturers: BCD increased to 10% from nil last year – Better pricing will enable further volume growth.

Final Comments

As expected, the Finance Minister delivered a Bill with highlights least expected by the Economic Pundits and Forecasters. Focusing on strengthening fiscal maths, credibility of the Budget estimates, has gone up, save for the ever-ambitious Divestment target. Revenue collections are modest and for a welcome change may be higher than the Budgeted at the year end, if the current economic recovery is not interrupted by a spike in the reported Covid cases.

The baton now shifts to RBI, to manage the delicate issue of smoothening any ruffled feathers of a nervous Bond market. This would be essential given the steady and large debt raising throughout FY22. The weight of debt issuance and the ugly specter of inflation remain the two biggest negatives, which could derail, even these modest FY22 estimates.

From an equity perspective, no new tax measures, focus on capital spending to boost infrastructure spend are the key positives. The use of Custom duty to “nudge/push” for domestic manufacturing is a clear extension of the ambitious PLI schemes announced over the last few quarters. This Government, it appears, is determined to raise the share of manufacturing, while achieving the goal of India becoming a $5 trillion economy. In past budgets, the devil, has always been in the fine print. On that note, nothing alarming has yet been spotted!

For now, let the beaten-up domestic cyclicals / “value” sectors enjoy their time in the sun!

Disclaimer:

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

The Disclosures of opinions/in house views/strategy incorporated herein is provided solely to enhance the transparency about the investment strategy / theme of the Scheme and should not be treated as endorsement of the views / opinions or as an investment advice. This document should not be construed as a research report or a recommendation to buy or sell any security. This document has been prepared on the basis of information, which is already available in publicly accessible media or developed through analysis of IDFC Mutual Fund. The information/ views / opinions provided is for informative purpose only and may have ceased to be current by the time it may reach the recipient, which should be taken into account before interpreting this document. The recipient should note and understand that the information provided above may not contain all the material aspects relevant for making an investment decision and the security may or may not continue to form part of the scheme’s portfolio in future. Investors are advised to consult their own investment advisor before making any investment decision in light of their risk appetite, investment goals and horizon. The decision of the Investment Manager may not always be profitable; as such decisions are based on the prevailing market conditions and the understanding of the Investment Manager. Actual market movements may vary from the anticipated trends. This information is subject to change without any prior notice. The Company reserves the right to make modifications and alterations to this statement as may be required from time to time. Neither IDFC Mutual Fund / IDFC AMC Trustee Co. Ltd./ IDFC Asset Management Co. Ltd nor IDFC, its Directors or representatives shall be liable for any damages whether direct or indirect, incidental, punitive special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information.