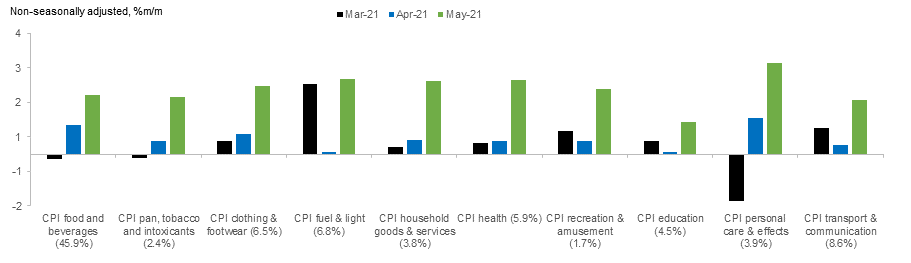

The reflation theme emphatically announced itself to the Indian shores with the set of inflation prints for May. Thus WPI printed a multi-decade high of almost 13%, even as it was quite within the bound of expectations. CPI on the other hand overshot expectations by almost a full 100 bps, printing a jaw-dropping 6.3% for May. The charts below captures which components contributed most to this increase in CPI.

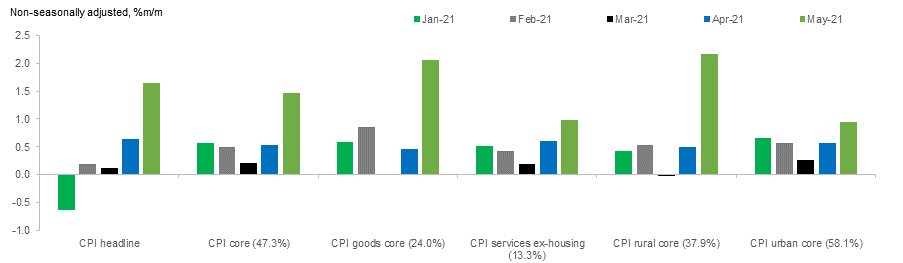

Source: CEIC, IDFC MF Research. Note: Numbers indicated in brackets are weights in CPI.

As is evident, the rise is broad-based and reflects both imported components of inflation as well as possibly renewed rigidities associated with the recent lockdowns (reminiscent of what had happened last year). Also reflective of last year, there could have been data collection issues in May. Nevertheless, the print is not only a substantial negative surprise on its own but also serves to significantly restate forecasts of average inflation for the full financial year. These are still in a wider range of around 5.4 – 6% for now reflecting different assumptions by individual forecasters on how much and how soon some of the recent upward effects begin to unwind. But whichever way one slices it, it is quite likely that the average for FY22 will now be likely significantly higher than the RBI’s most recently estimated 5.1%.

The RBI’s Dilemma and Bond Market Implications

As discussed in detail in our post policy note (https://idfcmf.com/article/4807), RBI now links bond yield and corporate bond spreads much more closely to its assessment of the general state of local financial conditions. Its desired stance on the relative looseness in financial conditions is in turn linked to its assessment of the growth versus inflation tradeoff. Thus post the first wave as activity was rebounding strongly, the central bank was transitioning to a business as usual dovishness. This meant that it was still supporting the bond market even intensifying its efforts when yields ‘came undone’, but largely guiding an orderly evolution of the yield curve. With the second wave, it reverted to a more aggressively dovish approach and this started reflecting in its more aggressive bond market interventions as well. This was evidenced in RBI seeming to dictate almost the level of the 10 year bond yield over the past few weeks.

The May CPI print will likely on the margin push up the importance of inflation in the growth versus inflation tradeoff for RBI. This doesn’t necessarily mean that the central bank will start to respond to this right-away. However, the bond market may step up speculation with respect to the shelf-life for RBI’s current ultra-dovishness. This may make the task of dictating yields to the market that much more difficult for the central bank. At any rate, in our base case view RBI would have started to dial back on its level of intervention at some point and we were budgeting for a gradual rise in yields overtime. Also it makes sense to assume in the base case that if re-opening were to progress smoothly, RBI will re-initiate its path to normalization especially now as the comfort with CPI is that much lower. This will probably take the form of more longer term variable reverse repo rate (VRRR) auctions to begin with and then the start of gradual reverse repo rate hikes. At this juncture we would think the first such hike will happen somewhere in the October – December period of this year.

The Cost Versus Benefit of Flexibility

An enduring theme of this cycle has been the extra-ordinary steepness of the yield curve, even at intermediation duration points (maturity segments of 3 – 6 years as an example). This has meant that the cost of running cash has been significant. As an example, the cost of running cash instead of the benchmark 5 year government bond is approximately 4 – 5 bps a month of carry loss on the bond. This means that if you sold the bond today and bought it back around 15 bps higher after 3 months, you would have done no better than continuing to hold on to the bond over this period of 3 months when its yield rose by 15 bps. This also allows one to pick the relevant duration points on the curve where the carry adjusted for duration risk seems the most optimal.

While the above quantifies the cost of keeping cash, one can also not deny the flexibility afforded in keeping some cash. The world is almost in an analytical black-box for now as far as predicting economic data is concerned. Take the case of the US. An unprecedented series of fiscal stimuli will yield economic growth far in excess of the long term potential growth rate for this year and next. The economy is re-opening rapidly and consumers have substantial savings to spend. On the other side, the economy has already seen peak stimulus and it is likely that a significant part of the excess savings goes into retiring debt and is retained as precautionary buffers for the future. It is also true that both inflation expectations as well as bond yields in the US haven’t responded to recent higher than expected inflation prints.

Or take India and RBI. The ‘K’ shaped impact of the virus, especially after the second wave, has caused (basis anecdotal evidence) widespread damage to incomes and purchasing power and will no doubt increase marginal propensity to save for wide sections of the population. Also one has to remember the context: growth was already weak in the run up to Covid and the total fiscal response in India has been relatively much more nuanced so far as compared with many other nations around the world. These may be working to keep RBI focused on growth for now, but the awkward CPI print will make that focus that much harder to keep.

Bond Strategy

It is partly because of these pushes and pulls, both from point of view of the utility of keeping cash and the cost of it as well as of prospects of imminent imported tightening and the arguments against it, that a ‘barbell’ approach seems to make sense. This is something we have spoken of many times before. It entails weighing intermediate duration exposure with very near end (cash or almost cash exposures). This allows for exploiting the steepness on the curve while retaining some flexibility with oneself.

Over the past few days, and after evaluating the pushes and pulls as discussed above, we have been raising the level of cash in our actively managed bond portfolios. We wanted to create flexibility given the global data black-box while at the same time wanting to get the timing right owing to the significant costs of holding cash. The recent dip in bond yields reflecting RBI’s heightened commitment over the past few months, finally swung us into action. While we had no great insight on expecting a higher CPI print, it made logical sense to get most of it done before the event risk of the inflation print. As on 14th June’21, our actively managed bond and gilt funds have cash levels between 20% – 35%. As always we will continually re-examine this in light of incoming information and as our views evolve. It is to be noted that, as discussed in detail above, this is to retain flexibility in positioning and our view remains the same with respect to what duration points make the most sense for investors in a bar-bell framework.

Disclaimer:

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

The Disclosures of opinions/in house views/strategy incorporated herein is provided solely to enhance the transparency about the investment strategy / theme of the Scheme and should not be treated as endorsement of the views / opinions or as an investment advice. This document should not be construed as a research report or a recommendation to buy or sell any security. This document has been prepared on the basis of information, which is already available in publicly accessible media or developed through analysis of IDFC Mutual Fund. The information/ views / opinions provided is for informative purpose only and may have ceased to be current by the time it may reach the recipient, which should be taken into account before interpreting this document. The recipient should note and understand that the information provided above may not contain all the material aspects relevant for making an investment decision and the security may or may not continue to form part of the scheme’s portfolio in future. Investors are advised to consult their own investment advisor before making any investment decision in light of their risk appetite, investment goals and horizon. The decision of the Investment Manager may not always be profitable; as such decisions are based on the prevailing market conditions and the understanding of the Investment Manager. Actual market movements may vary from the anticipated trends. This information is subject to change without any prior notice. The Company reserves the right to make modifications and alterations to this statement as may be required from time to time. Neither IDFC Mutual Fund / IDFC AMC Trustee Co. Ltd./ IDFC Asset Management Co. Ltd nor IDFC, its Directors or representatives shall be liable for any damages whether direct or indirect, incidental, punitive special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information.