The dramatic geopolitical developments of the past couple of weeks, and the consequent commodity price shock to the world, represent in some sense the manifestation of almost a tail risk event. It is hard, therefore, to run this through the traditional prism of macro-economics. While the risk of egg on face is inherent in making predictions, doing so in times like these is almost the equivalent of a face chasing after an egg. A better way to approach then is just in context of general market signals and what information they are providing to update one’s underlying macro-framework for the times. This is the attempt below.

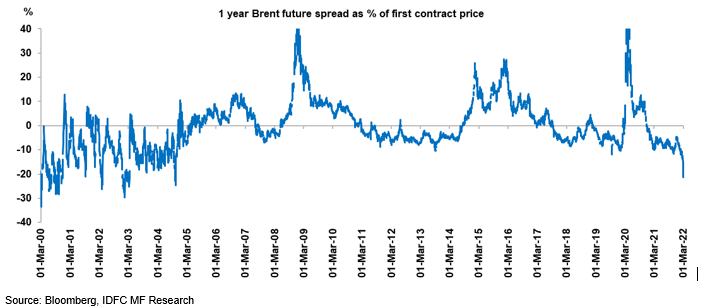

A good way to think about this shock is in terms of one’s ‘order of worries’ before this shock struck and then examine how this order may be modified/accentuated as the new dynamics flow through. Starting off, one has to note that most central banks will treat this as a one time shock and worry more about second order effects from the perspective of monetary policy setting. Thus it is mainly the risk of the large commodity price shock seeping into generalized, sustained product price and wage changes that they will want to guard against. This is important as monetary policy acts with a few quarters’ lag. Also, there is little that it can do to contain the first order impact emanating from a supply shock. Finally, monetary policy has to be also alive to the growth impact of a shock like this down the line. This again leads back to the starting point of the order of worries. What also needs attention is that even the commodity curve gets disrupted in times like these as is shown in the chart below which shows one year forward oil now at substantial discount to spot prices (note future oil price also ordinarily has a cost of carry built in). Thus strictly speaking, and as per the forward curve, the shock isn’t as large as just what the spot prices reflect.

The US Worry List

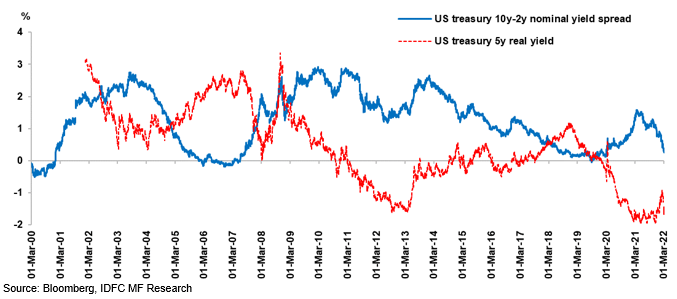

In the case of US, the Fed’s number one worry since late last year has been inflation; and for good reason. Not only is the headline print worrisome (CPI at 7.5% for January reading) but the breadth is also of concern. Thus the re-achievement of 2% over a reasonable time horizon was looking like a matter of more and more concern, thereby leading markets to price in seven rate hikes in 2022 alone till very recently. The Fed Chair hadn’t pushed back against any of this, given the backdrop. The geo-political shock has taken out approximately one rate hike from this expectation, even as inflation expectations have climbed further reflecting the steep rise in commodity prices. What is quite noteworthy is that even 5 year inflation expectations have risen 25 – 30 bps, which seems a bit much given the immediate nature of the commodity shock. This has led to real 5 year yields turning substantially further negative during this period. However, US yield curve has continued to flatten with the spread between10 year and 2 year sovereign yield currently at less than 25 bps, the lowest since early 2020. These two aspects are captured in the chart below

As can be seen, it is quite notable compared with history to have such a flat yield curve at this negative a real 5 year yield. Prima facie, this represents an uncomfortable situation for the Fed insofar that it suggests relative stickiness of inflation even as it indicates that the ability to hike over multiple years will dissipate. The same is seen in market pricing on rate hikes, where almost all hikes are now expected in 2022 itself with almost nothing in subsequent years. It is to be noted that this market narrative is quite different from a multi-year solid growth narrative thereby allowing a long period of policy normalization. However, it is more consistent with our own view that growth in developed markets has been ‘purchased’ via an unsustainably large fiscal stimulus, without really changing the underlying longer term trend rates. Hence, as this stimulus fades so would the heady growth environment thereby presumably making central banks more cautious to hike even as inflation may take longer to re-achieve previous comfort zones. The ongoing commodity shock, if anything, accelerates the slowdown. In a word, market curves could be beginning to price in the dreaded ‘stagflation’ scenario.

India’s Case

Starting off one has to acknowledge that its hard to underplay the macro worries that this latest commodity shock poses for India. The table below summarizes the likely impact on key variables in our assessment.

It is to be noted that our base forecasts in the above table are somewhat different from RBI. Thus for example, RBI forecasts a lower FY23 CPI and hence may not see a likely breach of its 6% target in the year ahead. It is also possible that some of this pressure is absorbed by the fiscal as well. While this will have its own set of worries for the bond market, the central bank may feel safer about defending the top end of the CPI target range. However, no matter how one cuts it, the new trajectories on CPI and current account are decidedly going to be in uncomfortable zone.

It is here that RBI’s order of worries merits a closer look. At the top of its list has been concerns on the robustness of growth. As at last update, the central bank had continued to find room to address this by keeping the accommodative guidance firmly in place. To be fair, this was possible since its inflation forecast saw us approaching an inflection point and was projected on a downward path through all of FY23. Deputy Governor Patra’s assessment was overwhelmingly in this direction. In particular the paragraph from the recent minutes that had stood out for us was this:

“Monetary policy is an instrument of stabilisation. Its role is to align demand with supply, not the other way round. When inflation is driven by demand, monetary policy can stabilise inflation and growth. Monetary policy cannot play its stabilization role when inflation is the result of supply constraints. So central banks have a choice: either accept higher inflation for some time or be prepared to be accountable for destroying demand.”

He was also fairly critical of several global central banks, saying that monetary policy authorities “in several parts of the world look at inflation in the rear-view mirror in which objects can look bigger than they are and they prepare to normalise and tighten. If they looked forward, they would sight a falling trajectory of inflation”. Presumably the reference here was to the developed market banks since the very next statement dealt with the spillover effects : “Other countries have to brace up for shock waves from spillovers”. The conclusion here was put quite bluntly : “Overall, I regard monetary policy chasing inflation instead of anticipating it as the main factor weighing down on global growth prospects.”

The working assumption here is that Dr. Patra’s analysis and broad leanings continue to resound with the effective majority of the monetary policy committee (Governor and one external member). Also, since a large part of policy is being conducted outside of the committee, the views of RBI leadership matter more now than they otherwise would in a more normal setting. While in all fairness RBI’s most recent analysis would not have accounted for this latest commodity price shock, the underlying framework as presented by the Deputy Governor may still very well be in play. Thus while the forecasted momentum on CPI may no longer be as benign, the shock is still a supply side one. While external account finds mention, it didn’t seem like a large consideration for now with RBI. The central bank leadership has taken pains to explain that the underlying settings in India are quite different from the US and that we needn’t follow the policy setting there. Furthermore, our large forex buffers are meant to offer some protection against potential spill over risks. Again, this characterization is unlikely to change.

The base case then is that despite macro-economic challenges having gone up in the near term, the bar for a substantial incremental hawkish pivot from RBI still remains somewhat high, in our view. This is especially true as growth headwinds will likely further increase with this new shock. In our forecasts presented in the table above, a 6%handle growth outcome for F2Y23 is now very much in the realm of the possible.

Market Micros

There have been two incremental developments of note in the Indian bond / money markets. First, banks have now become more accustomed to the new variable rate reverse repo (VRRR) regime. Consequently, both the volatility and the elevation in the overnight deployment rates have eased generally. Second, the market has loudly and clearly accepted RBI’s unequivocal message with respect to its reaction function (no line of sight on actual meaningful lift to the effective overnight rates). A combination of these has led to reasonably strong demand in rates up to the 2 year point on the curve. While there has been some pressure lately on money market rates owing to a revised treasury bill calendar and stepping up of CD/CP issuances, these have been comfortably absorbed thus far. This market behavior has opened up the spread between 4 year and 2 year government bond yields to a comfortable 110 bps or so. In line with our often expressed view before, we believe that this spread is more ‘playable’ and can be looked at as providing some relative cushion to the 4 year yield. As against this the 75 bps spread between 10 year and 4 year is probably too thin and certainly cannot be played upon with any degree of certainty given the huge supply of duration lined up ahead.

We had gone significantly into cash / cash equivalents in our active managed bond and gilt funds around mid of February. We had mentioned valuations in relation to the aggressive Fed pivot, the heightened geopolitical risks, and local bond supply issues (https://idfcmf.com/article/7131 ). We had also reiterated that the underlying framework, including which tenor of bonds we prefer, remained largely the same. Since then yields in our preferred segment (4 – 5 years) have risen approximately 25 – 30 bps. This is despite the above two dovish developments mentioned, as geopolitical risks have fructified. We have also seen somewhat larger pressure in the 4 – 5 year segment thereby leading to some steepening versus 2 year and some flattening versus 10 year. This has further increased the appeal for the 4 – 5 year segment to us, relatively speaking.

In what may seem a somewhat counter-intuitive move in the midst of a very uncertain global narrative, we have redeployed most of the cash / cash equivalent in our actively managed bond and gilt funds. This is obviously not without risks, and embedded here (alongside all the analysis presented above) is a hope that the very large commodity price swings witnessed over the past few days begin to calm down gradually. To be clear, we do believe that the ‘floor prices’ on various commodities is now higher than before and we still don’t expect to make any mark-to-market gains given this and the large bond supply calendar ahead. However, as discussed many times before, the extra-ordinarily steep yield curve levies a very large penalty on running cash. The re-deployment of cash partly is in appreciation of this aspect, partly reflecting the sharp short period sell off in bonds in our preferred segment, and partly is the sum of the analysis presented above.

Disclaimer:

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

The Disclosures of opinions/in house views/strategy incorporated herein is provided solely to enhance the transparency about the investment strategy / theme of the Scheme and should not be treated as endorsement of the views / opinions or as an investment advice. This document should not be construed as a research report or a recommendation to buy or sell any security. This document has been prepared on the basis of information, which is already available in publicly accessible media or developed through analysis of IDFC Mutual Fund. The information/ views / opinions provided is for informative purpose only and may have ceased to be current by the time it may reach the recipient, which should be taken into account before interpreting this document. The recipient should note and understand that the information provided above may not contain all the material aspects relevant for making an investment decision and the security may or may not continue to form part of the scheme’s portfolio in future. Investors are advised to consult their own investment advisor before making any investment decision in light of their risk appetite, investment goals and horizon. The decision of the Investment Manager may not always be profitable; as such decisions are based on the prevailing market conditions and the understanding of the Investment Manager. Actual market movements may vary from the anticipated trends. This information is subject to change without any prior notice. The Company reserves the right to make modifications and alterations to this statement as may be required from time to time. Neither IDFC Mutual Fund / IDFC AMC Trustee Co. Ltd./ IDFC Asset Management Co. Ltd nor IDFC, its Directors or representatives shall be liable for any damages whether direct or indirect, incidental, punitive special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information.