Union Budget – 2022-23 largely revolves around the financial system where the overall, macro-economic stability indicators suggest that the Indian economy is well placed to take on the challenges of 2022-23. A reason that the Indian economy is in a good position has been the unique response strategy of the Central Government. Rather than pre-commit to a rigid response, Government of India opted to use safety-nets for vulnerable sections on one hand while responding iteratively based on Bayesian-updating of information.

The broad theme for the Budget is structured on a Masterplan that will encompass the 7 engines of economic transformation:

· PM Gati Shakti

· Inclusive Development

· Productivity Enhancement

· Sunrise Opportunities

· Energy Transition

· Climate Action

· Financing of investments

BUDGET MATH:

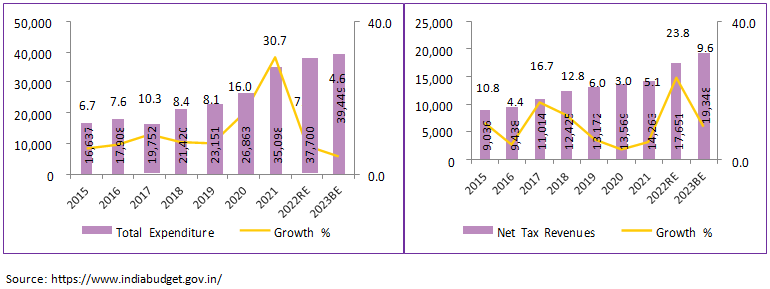

· The aggregate fiscal construct of the FY23 Union Budget reflects higher-than-expected conservatism with a very modest expenditure expansion of 4.6% at Rs 39.45tn. The emphasis continues to be on attempts to crowd-in private capital expenditure by continued acceleration of government capital outlay.

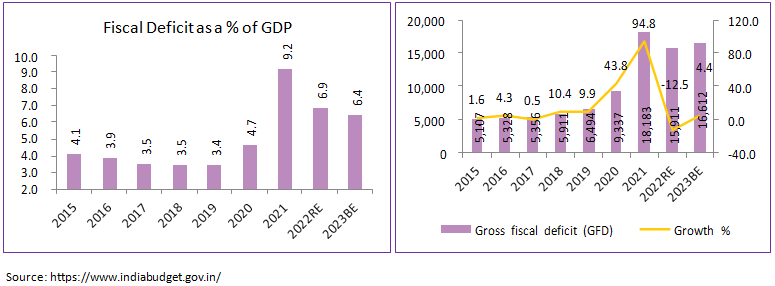

· Fiscal deficit FY23BE at Rs 16.61tn is merely an expansion of 4.5% over FY22RE; as a ratio of GDP it is projected to decline to 6.4% from 6.9% in FY22. But more importantly, reflecting the cutback in revenue spending, the revenue deficit at Rs 9.9tn is budgeted to decline by 9% YoY or to 3.8% of GDP from 4.7% in FY22RE.

· Revnue expenditure, which constituted 84% of total expenditure in FY22RE at Rs 31.7tn, is slated to decline to 81% contribution in FY23BE at Rs 31.95tn, which is flat on YoY basis (0.9% YoY). Reflecting an even more conservative view on consumption spending.

· Capital outlay for FY23 is budgeted at Rs7.5tn, which is a growth of 24.6% over FY22RE of Rs 6.6tn in FY22. After including internal and extra-budgetary resources (IEBR) of public sector enterprises (PSEs), the actual net capex is budgeted to grow by a modest ~6.2%.

· The assumption on disinvestments of Rs650bn in FY23BE is much looks more reasonable. Even the FY22RE has been revised downwards to Rs780bn. Collections from Spectrum auction (Rs 528bn) is on the higher side, given that telecom companies are pressing for reduction in 5G prices. Dividend pay-outs from RBI (Rs 739bn) and PSU companies (Rs 400bn) appear reasonable.

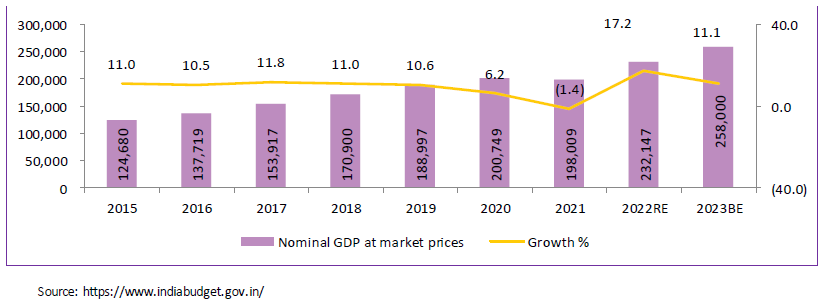

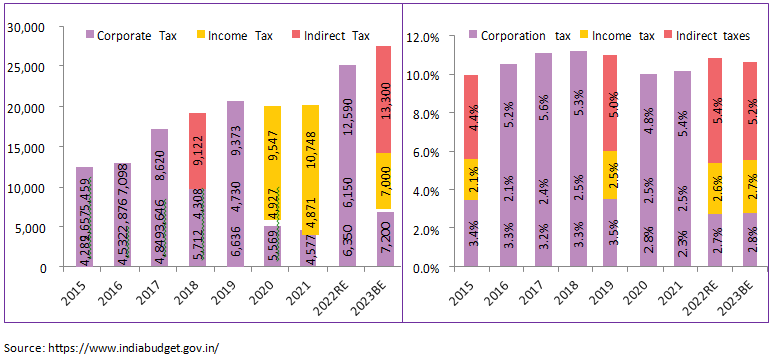

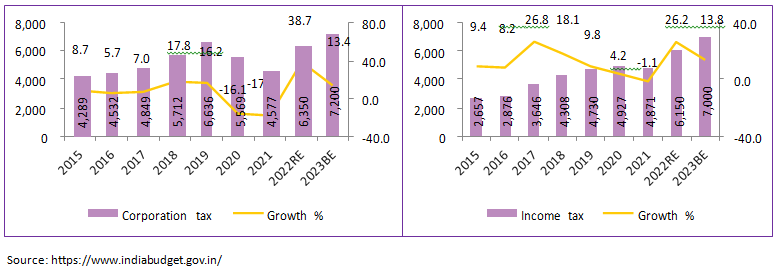

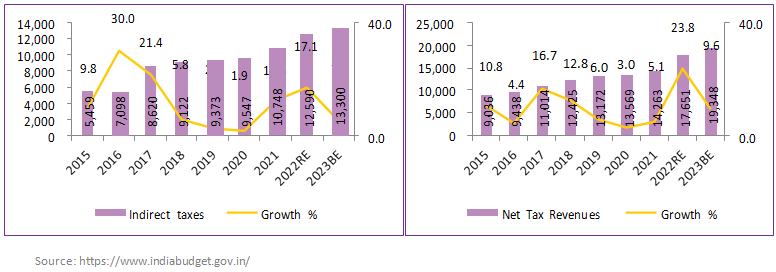

· With nominal GDP forecasted to grow at ~11.1%, revenue estimates look far more modest as compared to the past. The corporate tax collections at ~13% growth appears achievable. Even Indirect tax forecast at 6% in FY23BE is lower than the nominal GDP growth rate.

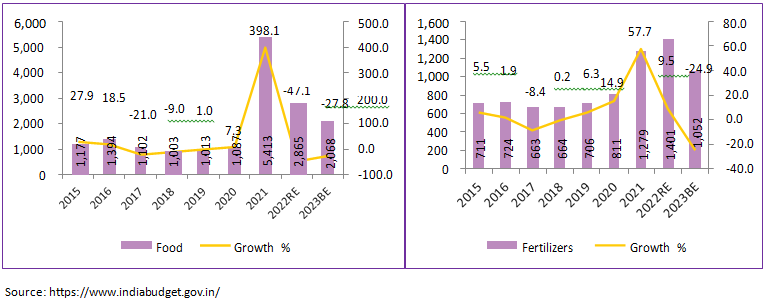

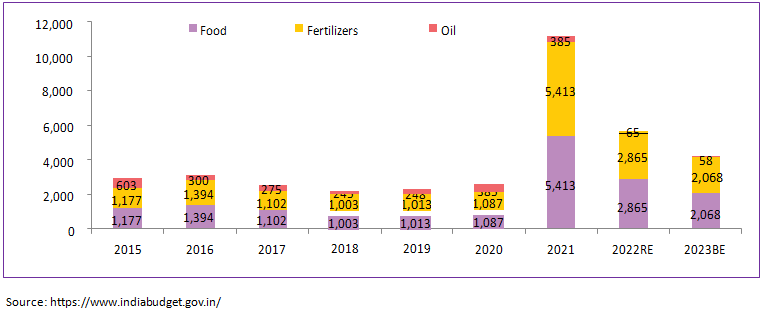

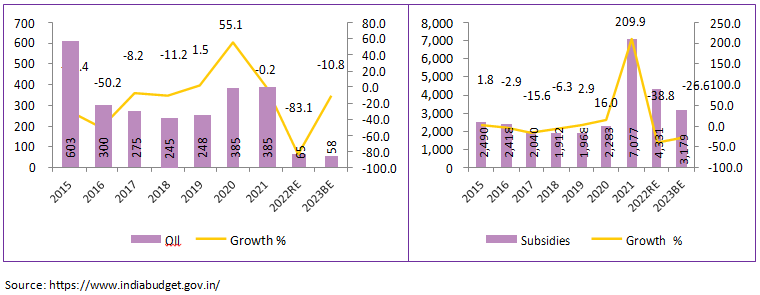

· Food subsidy had sharply increased due to reclassification of off-balance sheet items (loans to FCI) as a part of the regular budget and disbursement of free food grains during the pandemic period. With easing of pandemic and reduction of distribution of free food grains, Food subsidies have come down by 28%in FY23BE.

· Last year budget had cleared all the pending Fertilizer subsidy and hence FY23BE has reverted to the normalized allocation of Rs 1,052bn.

· India’s response to fiscal stimuli in the throes of the pandemic was more “measured” as compared to the developed countries like USA, Germany and Japan. Outlay on MNREGA which was the preferred route in the stimulus has “normalized” to Rs.73,000cr for FY23BE vs Rs 98,000cr in FY22RE which is 25.5% reduction in allocation.

Other Key Snippets:

· Infrastructure and Capex

· Extension of PLI scheme for data centers and warehousing is also targeted to encourage domestic manufacturing and commercial real estate

· The emphasis on Gati Shakti reflects potential gains for logistics companies at large, even as it creates competition for existing ones

· Increase in allocation for PM Awaas Yojna should aid volume traction for cement companies. Rs6tn allocated for providing access to tap water to 3.8 crore households – to benefit pipe companies

· Contracts for implementation of multimodal logistics parks at 4 locations through PPP. This would lead to a) higher volumes b) faster turn-around time c) Improved efficiency in operations

· Digital and Banking

· The other thing that is worth noting is acknowledgment that digital currencies are making significant inroads into the Indian markets. It is therefore proposed to introduce digital rupee using blockchain and other technology to be issued by the Reserve Bank of India starting, 2022 and 2023

· Sovereign green bonds will be part of government’s borrowing program in FY23 where proceeds to be deployed in public sector projects

· Issuance of E passports using embedded ship and futuristic technology to be rolled out in 2022- 23 to enhance the convenience for the citizens in their overseas travel

· Agriculture

· Chemical-free natural farming to be promoted in India – a negative for manufacturers of pesticides and related agri inputs

· Oil OMCs – Unblended petrol to attract Rs 2/lt of additional excise duty from Oct-22 – OMCs will have to pass this on to consumers as blending is uneven across the country based on feedstock availability.

· Telecom – Spectrum auction to be conducted in FY23 for the rollout of 5G mobile services by private telecom providers. Scheme for design led manufacturing to be launched under PLI scheme to enable affordable broadband and mobile communication in rural and remote areas.

· Auto – An EV battery swap policy to be announced during the year with interoperability standards to boost EV ecosystem.

· Defense capex spending increased 9.7% to Rs1.52tn. Importantly, positive is that 68% of the capital procurement budget will be earmarked for domestic industry in FY23BE v/s 58% in FY22RE.

· Allocation to Housing schemes stood at Rs480b, with a target to complete construction of 8m houses. This will continue to boost Cement consumption.

· Direct tax

· New provision to file updated return within 2 years of relevant assessment year in case of omission income

· A completely paperless, e-bill system will be launched by ministries for procurement

· Introduction of tax on income from digital asset transfers at 30% without claiming any form of deduction of expense other than cost of acquisition. Gift of cryptocurrencies to be taxed at the receiver’s end

Key Takeaways from Equity market perspective/span>

Overall from an equity market perspective, we believe the budget, has no unpleasant surprises while, there remains some room for further capex/spending push as the government is likely to overshoot its revenue targets

· The maximum surcharge rate on all long-term capital gains including units of equity and debt mutual funds have been brought down to 15% (from 37%) which would provide a much-needed boost to the mutual fund industry

· Digital Assets – Taxation on gains from the digital asset could help curb speculation and should help channelize savings into well-regulated long-term investments like Mutual Funds

Overall, the Budget gambit hinges crucially on hopes of improved traction in India’s private sector, quick revival in private capex, pick-up in employment, wage growth, and leveraging potential of the banking sector. The construct of the Budget is strongly geared towards fiscal consolidation, in the context of rising interest rates on elevated public debt, which at 92% of GDP (states and GoI) has risen to an 18-year peak. The risk to the gambit can arise from continued slack in consumption demand.

Source: https://www.indiabudget.gov.in/

Disclaimer:

The Disclosures of opinions/in house views/strategy incorporated herein is provided solely to enhance the transparency about the investment strategy/theme of the Scheme and should not be treated as endorsement of the views/opinions or as investment advice. This document should not be construed as a research report or a recommendation to buy or sell any security. This document has been prepared based on information, which is already available in publicly accessible media or developed through analysis of IDFC Mutual Fund. The information/views/opinions provided are for informative purposes only and may have ceased to be current by the time it may reach the recipient, which should be taken into account before interpreting this document. The recipient should note and understand that the information provided above may not contain all the material aspects relevant for making an investment decision and the security may or may not continue to form part of the scheme’s portfolio in the future. Investors are advised to consult their investment advisor before making any investment decision in light of their risk appetite, investment goals, and horizon. The decision of the Investment Manager may not always be profitable; as such decisions are based on the prevailing market conditions and the understanding of the Investment Manager. Actual market movements may vary from the anticipated trends. This information is subject to change without any prior notice. The Company reserves the right to make modifications and alterations to this statement as may be required from time to time. Neither IDFC Mutual Fund / IDFC AMC Trustee Co. Ltd./ IDFC Asset Management Co. Ltd nor IDFC, its Directors or representatives shall be liable for any damages whether direct or indirect, incidental, punitive special, or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.