Continued Policy focus on infrastructure spend supported with sharp increase in budgeted capital outlay

Union budget 2022-23 underlined continuation of last two / three years government policy focus. It has two clear objectives: 1. Achieving economic growth through infrastructure spends and 2. Enhancing manufacturing competence, both are complimentary. The spend targets are backed by step up in budgeted capital outlays as well as there is a conservativeness about the receipts, which would be seen positively.

Following are the key highlights on important segments of infrastructure.

Railways: Robust growth in capital expenditure ably supported by budgetary support

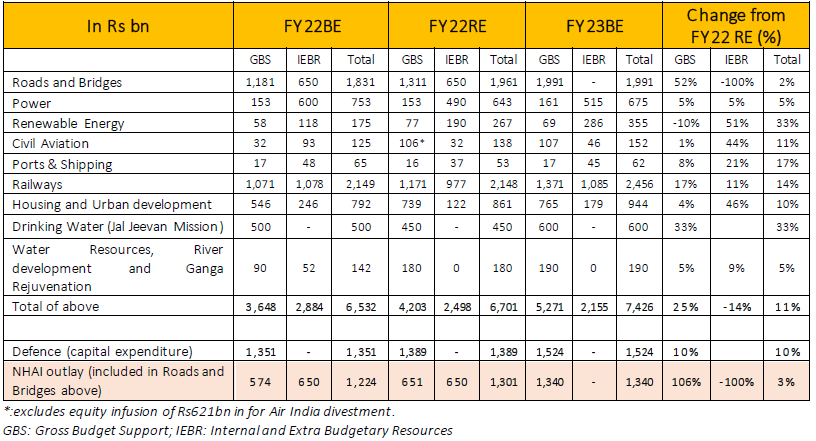

· Capital expenditure for FY22 maintained at Rs2.15 trn albeit with Rs100bn lower borrowings offset by increase in GBS. Budgeted to increase 14% to Rs2.45 trn in FY23.

· Of the incremental expenditure of Rs300bn, ~Rs200bn in funded by GBS and balance ~Rs100bn is funded by debt

· Overall borrowings of Railways budgeted at Rs1.08 trn up from Rs977bn in FY22 RE

· Strong growth in expenditure for new lines, doubling and investments in PSUs/SPVs (DFCC for instance)

· Drinking water (JJM) – FY22 RE at Rs450bn from Rs500bn BE. FY23 BE increased 33% to Rs600bn

· Housing and Urban Development (included metro rail) – FY22 RE at Rs861bn up from FY22 BE of Rs792bn. FY23 BE increased 10% to Rs944bn. GBS for Metro Rail flat at Rs190bn and for PMAY also flat at Rs480bn – indicating greater share of expenditure to be funded by states/lending agencies

· Defence capex – FY22 RE at Rs1.39 trn up from FY22 BE of Rs1.35 trn. FY23 BE increased 10% to Rs1.52 trn.

➢ If one goes by Chinese example both segments has potential for much higher spend that can provide strong stimulus for the economic growth. We expect the scale up in these segments to continue to pick up in coming years.

Roads and Highways:

· MORTH: FY22 expenditure increased from Rs1.83 trn BE to Rs1.96 trn RE. Marginal 2% growth to Rs2 trn in FY23.

· NHAI (included as part of MORTH): FY22 increased from Rs1.22 trn BE to Rs1.3 trn RE. 3% growth to Rs1.34 trn in FY23, however it is growing on an already high base.

· A part of this can may be explained by a likely dip in expenditure on land acquisition and corresponding increase in project expenditure as also lower capital requirement for NHAI due to HAM projects. At the same execution capacity of Indian infrastructure companies have improved substantially over the years.

MORTH: Ministry of Road Transport and Highways of India

Budgetary allocations in major infrastructure segments:

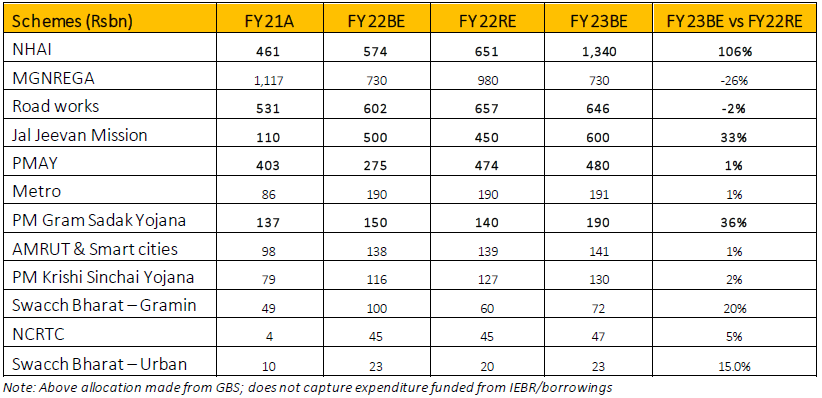

Outlay on major schemes:

Take Aways:

· Clear focus on transportation infrastructure, multi modal logistic parks, urban planning, as well as energy transition and it is backed by 35% increase in capital outlay to 7.5 lac crore from 5.5 lac crore is a key highlight of budget from infrastructure sector point of view

· The budget also emphasized on 25000 Km of National Highways and encouraging domestic industry participation in defense industry

· It reinforced continuing stance of govt of focusing on job creation through infrastructure development by focusing public infrastructure spending

Risk factors to the Infrastructure theme:

· Public expenditure remains strongest driver of the infrastructure development in country. While it has remained very strong for a long period, fiscal pressure at times has the potential to affect the spends

· Long gestation period for infrastructure projects is one of the key challenges. Longer time frame also require lower cost of capital for longer period of time

· The above results in some amount of cyclicality in the sector. Therefore, understanding the leverage and valuation discipline in sector investment is of paramount importance

IDFC Infrastructure Fund – Portfolio Stance:

The portfolio is built with an objective to monetize the infrastructure opportunity in India. Despite the argument of economic environment being slower, we believe that companies with a dominant market share and better cash flows would consolidate the opportunity going forward. The focus is on companies with a healthy balance sheet that could be beneficiaries of capital formation and can capture a large part of that revenue pool. The current portfolio includes companies from the Construction & Cement, Logistics segments, Industrials space, the Utilities, and Energy businesses.

The portfolio construction is agnostic to Style (growth/value/quality) or Market cap (large/mid/small), given the thematic nature of the fund. Further, the alignment of fund to its benchmark is also low, due to the concentration of higher order companies in the benchmark (~55% wgt. to large-caps). Refer the Quarterly Note-Dec2021 for more details on the fund.

Source: https://www.indiabudget.gov.in/

Riskometer:

IDFC Infrastructure Fund: An open-ended equity scheme investing in Infrastructure sector

Disclaimer:

The Disclosures of opinions/in house views/strategy incorporated herein is provided solely to enhance the transparency about the investment strategy/theme of the Scheme and should not be treated as endorsement of the views/opinions or as investment advice. This document should not be construed as a research report or a recommendation to buy or sell any security. This document has been prepared based on information, which is already available in publicly accessible media or developed through analysis of IDFC Mutual Fund. The information/views/opinions provided are for informative purposes only and may have ceased to be current by the time it may reach the recipient, which should be taken into account before interpreting this document. The recipient should note and understand that the information provided above may not contain all the material aspects relevant for making an investment decision and the security may or may not continue to form part of the scheme’s portfolio in the future. Investors are advised to consult their investment advisor before making any investment decision in light of their risk appetite, investment goals, and horizon. The decision of the Investment Manager may not always be profitable; as such decisions are based on the prevailing market conditions and the understanding of the Investment Manager. Actual market movements may vary from the anticipated trends. This information is subject to change without any prior notice. The Company reserves the right to make modifications and alterations to this statement as may be required from time to time. Neither IDFC Mutual Fund / IDFC AMC Trustee Co. Ltd./ IDFC Asset Management Co. Ltd nor IDFC, its Directors or representatives shall be liable for any damages whether direct or indirect, incidental, punitive special, or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.