How does one view markets at current levels? Should you view it in the context of last fiscal year returns – Nifty (Large cap index) up by 72%, Mid Cap index up by 102% and Small cap Index up by 126% or from January 1 2020, before the pandemic – up 21% for Nifty, 38% Mid Cap index and 38% Small cap Index? Either way it would be difficult to ignore the 29x trailing valuation or the two year forward P/E and valuations which are at the upper end of the historical band.

CY 2020 / FY 21 has been an unusual year, which can’t and shouldn’t be compared with “normal” years. Will economic growth in CY 21/FY 22 rebound with the same intensity as it is being forecasted now? How correct will these forecasters be, after their dismal CY 20 / FY 21 forecasts made at the end of April-June 2020 quarter last year?

The market moves have been nothing short of spectacular for this unusual year. After the fall in March, the markets bottomed on March 23, 2020 and have been practically been on a one-way ticket …

Source: Bloomberg

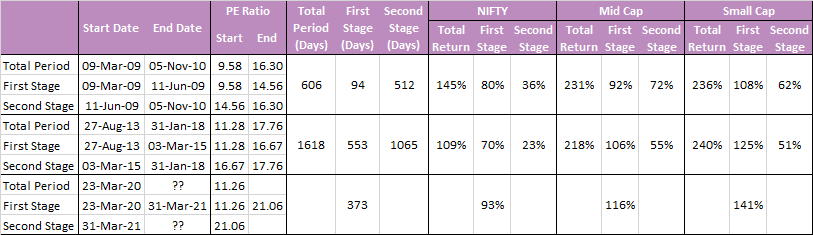

After such a resounding moved, how does one position oneself as an investor? We have two examples of recent market rallies – which may help us gather the courage to invest after phase I of the rally is over.

Boosted by the launch of QE (Quantitative easing) by the US Federal Reserve, markets shot up from March 2009 peaking in November 2010 (with an unexpected election result thrown in). During Phase I, as is the case with most Phase I rallies – market move was fast and furious, with most return coming from P/E re-rating rather than earnings growth. Usually broader market participation is visible.

Phase II: Market move is gradual with corrections, earnings revival or lack of it determines the length of this stage. P/E re-rating is limited in this phase of the market uptrend. Usually a prolonged disappointment in earnings growth ends the uptrend.

Clearly, we are in the Phase II of the uptrend, the middle overs of an ODI, (except as Howard Marks giving the baseball reference mentions, stock market is an endless Baseball match, for our reference, a limited overs ODI, where teams continue to play), to use a cricketing parlance.

Past market trends have shown that valuations by themselves may not lead to a correction, however, investor expectations of earnings growth if not met, have a bigger impact on the burden of high valuations and trigger stock market corrections. While, a few macro events dominate debate today – Inflation, commodity prices uptrend and US 10-year yields, earnings should be the key focus for investors going forward.

This gains even more importance, with March 2021 quarter earnings season just about to start. As investors, be ready for a drop in EBIDTA margins, which touched an all-time high in December 2020 quarter. The unsustainability of the previous quarter margins is a given. What will matter, if sales growth builds on the foundation of 9 months FY 21. Managements will try to shift investor focus from margin to absolute growth at EBDITA and PAT levels. Thankfully, low base effect of last year’s March and June quarters builds an easy base for the y-o-y comparison. Operational costs cut effected last year will also be watched with keen interest, were the savings of FY 21 structural or just tactical?

Also watch out for the “undesirable” second wave, not at all as benign and interesting to observe as a Mexican “wave”. Vaccination and its impact on numbers of cases is evident from two countries which have achieved over 50% adult vaccination – Israel and UK. Both have reported a sharp drop in number of new cases and hospitalization. The pace of vaccination, currently a shade below 6.5% of adults in India (those having taken the initial jab). The speed with which we cross 25%/33%/50% levels of successfully vaccinating the adult population, may have a direct bearing on how further will our economic trajectory be 7%/9%/11%!

Disclaimer:

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

The Disclosures of opinions/in house views/strategy incorporated herein is provided solely to enhance the transparency about the investment strategy / theme of the Scheme and should not be treated as endorsement of the views / opinions or as an investment advice. This document should not be construed as a research report or a recommendation to buy or sell any security. This document has been prepared on the basis of information, which is already available in publicly accessible media or developed through analysis of IDFC Mutual Fund. The information/ views / opinions provided is for informative purpose only and may have ceased to be current by the time it may reach the recipient, which should be taken into account before interpreting this document. The recipient should note and understand that the information provided above may not contain all the material aspects relevant for making an investment decision and the security may or may not continue to form part of the scheme’s portfolio in future. Investors are advised to consult their own investment advisor before making any investment decision in light of their risk appetite, investment goals and horizon. The decision of the Investment Manager may not always be profitable; as such decisions are based on the prevailing market conditions and the understanding of the Investment Manager. Actual market movements may vary from the anticipated trends. This information is subject to change without any prior notice. The Company reserves the right to make modifications and alterations to this statement as may be required from time to time. Neither IDFC Mutual Fund / IDFC AMC Trustee Co. Ltd./ IDFC Asset Management Co. Ltd nor IDFC, its Directors or representatives shall be liable for any damages whether direct or indirect, incidental, punitive special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information.